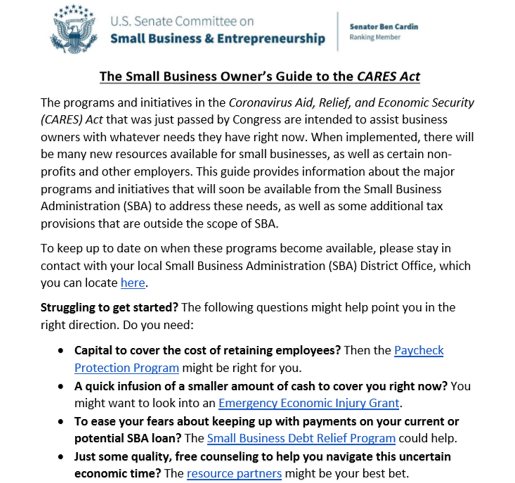

In response to the COVID-19 pandemic, Congress has passed far-sweeping legislation intended to assist individuals and businesses that have been adversely impacted by the virus.

The third piece of legislation, known as the “Coronavirus Aid, Relief and Economic Security Act” (CARES Act), provides $2 trillion in funding various relief measures. Included among the many provisions of the Act is the availability of loans from the Small Business Administration (SBA) some of which may qualify for conversion into grants which do not have to be repaid, if used for certain purposes, including to assist qualifying small businesses with providing compensation and benefits to their employees.

Lipson Neilson attorneys are studying the Act and will be here to assist our clients in understanding the various forms of relief and assistance under the Act, including navigating the SBA loan application process, and the administrative and record keeping requirements related thereto.

Among the potential benefits provided under Division A, Title I of the Act, entitled the “Keeping American Workers Paid and Employed Act” are the availability of SBA loans to qualifying businesses, that may be used to assist in covering:

- Payroll costs,

- Continued group health care benefits during period of paid sick, medical or family leave and insurance premiums,

- Employee salaries, commission, or similar compensations (subject to certain caps),

- Payments of interest on certain mortgage obligations,

- Rent,

- Utilities,

- Interest on any other debt obligations that were incurred before the covered period.

Subject to certain conditions and limitations, during a covered period, some of these loans will be without recourse, and will not require personal guarantees or collateral, to the extent funds borrowed are not commingled with other funds and are documented as having been utilized solely for the purposes identified above.

The typical fees associated with SBA loans when utilized in accordance with this Act are waived. A limited portion of the loan may even be subject to forgiveness, if certain conditions are met, with the balance repaid at a rate not to exceed 4%, and a maximum maturity of 10 years from the time that loan forgiveness is requested.

In addition, some borrowers may qualify for loan repayment deferral of not less than 6 months and not more than 1 year. Importantly, any portion of the loan that qualifies for loan forgiveness will not result in the typical federal income tax consequences generally associated with loan forgiveness.

There are other provisions specifically aimed at providing assistance to “women’s business centers”, those in the health care industry and other specifically target business segments.

There are time sensitive timelines for applying and qualifying for loans under the Act, as well as numerous conditions and restrictions set forth in this 854-page Act.